Never really understood how Blogger stats work. I have noticed this before - that when I stop posting, the number of subscribers goes up! Either someone is trying to tell me something or its those damn ghosts in the machine again...

Anyways, if there is anyway that it was missed...I have moved the blog to its own website at http://pazzomundo.com/. To subscribe simply click on the RSS icon in your browser navigation bar.

Wednesday, September 30, 2009

Sunday, September 27, 2009

Moving house - my very own website

Time has come to leave the nest - so long Blogger, thanks for all the help - you can find my new blog address at the following link:

http://pazzomundo.com/

(It's a work in progress...so don't expect too much...any feedback will be graciously accepted.)

http://pazzomundo.com/

(It's a work in progress...so don't expect too much...any feedback will be graciously accepted.)

Thursday, September 24, 2009

What was wrong with the FOMC minutes?

So the FOMC minutes were released, the market held firm until...well something spooked a steep sell-off into the close.

What happened? It wasn't as if there was anything particularly pointed in the minutes. More a summary of the timidity of the recovery and that policy will need to continue to be supportive. (You can read it here.) But there was something in there - I read it as a restatement of the 'exit policy'.

And there's the rub. We have reached the point where the patient is going to leave rehab - that means no more intravenous drips, no more call button and, maybe to the positive, no more hospital food. It doesn't mean that there won't be attentive nurses dropping by to offer some comfort but it is homecare for us now.

Consider the following charts of the Fed's open market operations that are designed to pump new money into the system. First up the agencies where the Fed has committed to purchasing up to $200bn of agency debt and $1,250bn of agency MBS by the end of Q1 in 2010 (as opposed to the end of this year as previously foreshadowed):

.jpg)

.jpg)

In both cases, we are over half way towards to the final purchase volume, but with the slowing down of purchases, MBS acquisitions in particular will be at a markedly lower rate.

(Here I've simply assumed that the balance will be spread evenly across the period to the end of March.)

Now to the treasury purchases that to date at least seem to have had a disproportionately larger impact on risk markets (it'd be great to have a correlation analysis between these tenders and movements in the equities markets but it's beyond my time constraints). Here we are at the tail end of the planned purchases:

.jpg)

The Fed can't print money indefinitely. It needs to engineer an exit strategy. The withdrawal of the pump priming treasury POMO is designed to achieve exactly this.

Without the artificial bid, the markets need to stand on their own feet. Given the economic backdrop that prevails, this is not consistent with the return of the raging bull. Rather expect it to be a catalyst for a sell-off as the market seeks to find the 'new' floor. If there isn't one - expect the Fed to step up again - with POMO part II.

Finally, out of curiosity I looked at the level of acceptances as against the volume of stock submitted through the Treasury POMO. I wasn't hoping for much - but was interested to see whether there was a loose correlation with the March lows and recent activity:

It was inconclusive. The volume of stock offered into the tenders has averaged around $20bn per tender (with pretty large volatility around this - which could be for any number of reasons). At face value, there does seem to be lower levels of acceptance around the March lows. And, interestingly, recent history has retraced to these types of levels. Not sure it means much, but might be worth keeping an eye on.

What happened? It wasn't as if there was anything particularly pointed in the minutes. More a summary of the timidity of the recovery and that policy will need to continue to be supportive. (You can read it here.) But there was something in there - I read it as a restatement of the 'exit policy'.

And there's the rub. We have reached the point where the patient is going to leave rehab - that means no more intravenous drips, no more call button and, maybe to the positive, no more hospital food. It doesn't mean that there won't be attentive nurses dropping by to offer some comfort but it is homecare for us now.

Consider the following charts of the Fed's open market operations that are designed to pump new money into the system. First up the agencies where the Fed has committed to purchasing up to $200bn of agency debt and $1,250bn of agency MBS by the end of Q1 in 2010 (as opposed to the end of this year as previously foreshadowed):

.jpg)

.jpg)

(Here I've simply assumed that the balance will be spread evenly across the period to the end of March.)

Now to the treasury purchases that to date at least seem to have had a disproportionately larger impact on risk markets (it'd be great to have a correlation analysis between these tenders and movements in the equities markets but it's beyond my time constraints). Here we are at the tail end of the planned purchases:

.jpg)

With $10bn left in the kitty, that is to be spent by the end of October, this liquidity injection is all but over.

The Fed can't print money indefinitely. It needs to engineer an exit strategy. The withdrawal of the pump priming treasury POMO is designed to achieve exactly this.

Without the artificial bid, the markets need to stand on their own feet. Given the economic backdrop that prevails, this is not consistent with the return of the raging bull. Rather expect it to be a catalyst for a sell-off as the market seeks to find the 'new' floor. If there isn't one - expect the Fed to step up again - with POMO part II.

Finally, out of curiosity I looked at the level of acceptances as against the volume of stock submitted through the Treasury POMO. I wasn't hoping for much - but was interested to see whether there was a loose correlation with the March lows and recent activity:

It was inconclusive. The volume of stock offered into the tenders has averaged around $20bn per tender (with pretty large volatility around this - which could be for any number of reasons). At face value, there does seem to be lower levels of acceptance around the March lows. And, interestingly, recent history has retraced to these types of levels. Not sure it means much, but might be worth keeping an eye on.

Wednesday, September 23, 2009

New highs and key reversals

Some signs that last night mark's an important inflection point for the rally...the Nasdaq, S&P500 and Russell all tripped over in the last 90 minutes of the day...and marked out key reversals on a daily basis.

.jpg)

.jpg)

.jpg)

In my experience, key reversal's (in this case, a new high but a close lower than the low of the previous day) have good form. They are particularly canny at picking a change in trend if they occur on a weekly basis (as was the case in stocks like MQG at the lows back in March) but let's not get ahead of ourselves.

The global risk trade rally is on its last legs - time to arc up the size of the short...

I've been working through the FOMC minutes - come back separately with why I think a relatively innocuous statement sparked a sell-off.

.jpg)

.jpg)

.jpg)

In my experience, key reversal's (in this case, a new high but a close lower than the low of the previous day) have good form. They are particularly canny at picking a change in trend if they occur on a weekly basis (as was the case in stocks like MQG at the lows back in March) but let's not get ahead of ourselves.

The global risk trade rally is on its last legs - time to arc up the size of the short...

I've been working through the FOMC minutes - come back separately with why I think a relatively innocuous statement sparked a sell-off.

Tuesday, September 22, 2009

Sector rotation

It's school holidays...games of squash and cluedo, trips to the zoo and other frivolities are the order of the day...

The volume of commentary calling for a correction (orderly or otherwise) is growing. While on one hand it meaningless noise, it does add to a general sense of foreboding. Longs are happy to sit on their hands, though the ripcord is never far from reach.

For mine, the Dec XJO puts I bought on this run up are still in play - on balance, I'm expecting a pullback to around the various moving averages around 4550. I'll trade against the Mar XJO puts if we get some meaningful volatility heading into the new year.

One shape in the charts that has caught my eye are the defensives. There is a general bid against some of these stocks that suggests that a rotation into these types of stocks could be in the offing. That would fit with a retracement scenario where investors take profit but look to stay in the market.

Have a look at TCL for example. It held the $4.00 level over recent weeks with rising volume and momentum divergence. It is testing its longer term downtrend. Think I'll look to pick some up over next week if it breaks higher (near term target $4.70)...

.jpg)

The volume of commentary calling for a correction (orderly or otherwise) is growing. While on one hand it meaningless noise, it does add to a general sense of foreboding. Longs are happy to sit on their hands, though the ripcord is never far from reach.

For mine, the Dec XJO puts I bought on this run up are still in play - on balance, I'm expecting a pullback to around the various moving averages around 4550. I'll trade against the Mar XJO puts if we get some meaningful volatility heading into the new year.

One shape in the charts that has caught my eye are the defensives. There is a general bid against some of these stocks that suggests that a rotation into these types of stocks could be in the offing. That would fit with a retracement scenario where investors take profit but look to stay in the market.

Have a look at TCL for example. It held the $4.00 level over recent weeks with rising volume and momentum divergence. It is testing its longer term downtrend. Think I'll look to pick some up over next week if it breaks higher (near term target $4.70)...

.jpg)

Thursday, September 17, 2009

A history of mean reversion

Following is a chart of the All Ordinaries from 1984 to the present with the 50 day and 200 day simple moving averages overlayed:

.jpg)

And here is a look at these same moving averages from a slightly different perspective - it's a chart mapping the percentage difference between the All Ordinaries and these moving averages over time:

.jpg)

Finally, had a quick look at the (even) longer term. Following is a chart of the All Ordinaries (in log format) from 1875:

.jpg)

.jpg)

.jpg)

And here is a look at these same moving averages from a slightly different perspective - it's a chart mapping the percentage difference between the All Ordinaries and these moving averages over time:

.jpg)

A couple of conclusions from these charts:

1) By this measure, March of this year was an absolute bargain.

2) We have now reached the other end of the spectrum where the market is trading over 10% above the 200 day MA. This doesn't happen often - and when it has (1987 pre-crash and then the post crash bounce and 1993 before interest rates got ratcheted up) the market has had some sort of pullback in the near term.

3) The flipside to this is that part of the 'mean reversion' is that the mean itself starts coming up to meet the market.

On the evidence of 1987, we could conclude that the market will probably correct from today's levels, but another crash is not in the making. It is more likely that the market will trade broadly sideways for the forseeable future.

One big difference between 1987 and now that could change this dynamic is that interest rates were an effective policy tool back then. Global interest rates plummeted post the crash and this kicked off a round of asset price inflation (that ultimately lead to our home grown property bubble). Will this work this time? Probably not - that is why central banks around the world are doing the QE two-step. On the evidence of the repricing of risk assets this does seem to be working. As we've noted before the real test is about to unfold as the QE is taken out of the system...

.jpg)

And the difference between the monthly average above and the rolling 12 month simple average of this average (sorry but it was the best I could do).

.jpg)

Speaks for itself really...

It's mine I tell you...

I think I look a little like Bjorn in this...or is it Benny...never could tell which was which...

What does a blow-off top feel like?

In a former life, when hormones and beer lust ruled the roost, I traded currencies in London hours out of Sydney. Staring at the screens from my monastic cell today, reminds me of those misbegotten days trying to guess where the squiggles are going to turn next...

A comment from a broker in London comes to mind, we are in the casino playing craps..."You play with fire sometimes"...he wasn't talking about my expertise at rolling dice but a mean reversion trade that I'm prone to putting on.

And that is where we are now. The market is running hard. It has all the hallmarks of the blow-off top. To be short at the wrong level hurts. Do you cut the position or add to to it?

What does a blow-off top feel like? When will exhaustion set in? And where will a retracement, assuming there is one, take us?

Going through them in turn...

What does a blow-off top it feel like?

1) It hurts - not only is the price running against you, the market scorns your views.

2) It's fast - adding to a position, at what you think is a good level, quickly runs against you.

When will exhaustion set in?

1) It's parabolic - prices can run, and typically do run, further than you expect.

2) The popularly accepted target level - the market psychology is one of trying to catch the last x% of the move. There is a feeling of certainty that the market will reach the given level (in our case, XJO to 5000). The buyers at current levels are looking to capture that last x% and then get out. The sellers are already set or too scared to jump in. The exits will be overcrowded as we approach the 'target' level.

Where will a retracement take us?

1) Buyers of the dip - the blow-off top will have sucked a lot of these reluctant buyers in for fear of missing the big trend. They will be the first to sell on a break of the up-trend.

2) To the last level where long term buyers were left hungry - Support will first appear where the under-invested but cautious investors are waiting. Logically this will be at the top of the head of the 'head & shoulders' that shall not be named.

So back to my broker, my response was that I'm looking for the market to come back to the trend.

I will add to the short as the 'popular target' approaches. At its simplest, the short trade is looking for a move back to longer term support. If we break lower from there so be it. If, against the wash of fundamental data, the market finds legs, I'm happy to go with that too. My experience suggests there is a trade to be made from betting against the parabolic move...

A comment from a broker in London comes to mind, we are in the casino playing craps..."You play with fire sometimes"...he wasn't talking about my expertise at rolling dice but a mean reversion trade that I'm prone to putting on.

And that is where we are now. The market is running hard. It has all the hallmarks of the blow-off top. To be short at the wrong level hurts. Do you cut the position or add to to it?

What does a blow-off top feel like? When will exhaustion set in? And where will a retracement, assuming there is one, take us?

Going through them in turn...

What does a blow-off top it feel like?

1) It hurts - not only is the price running against you, the market scorns your views.

2) It's fast - adding to a position, at what you think is a good level, quickly runs against you.

When will exhaustion set in?

1) It's parabolic - prices can run, and typically do run, further than you expect.

2) The popularly accepted target level - the market psychology is one of trying to catch the last x% of the move. There is a feeling of certainty that the market will reach the given level (in our case, XJO to 5000). The buyers at current levels are looking to capture that last x% and then get out. The sellers are already set or too scared to jump in. The exits will be overcrowded as we approach the 'target' level.

Where will a retracement take us?

1) Buyers of the dip - the blow-off top will have sucked a lot of these reluctant buyers in for fear of missing the big trend. They will be the first to sell on a break of the up-trend.

2) To the last level where long term buyers were left hungry - Support will first appear where the under-invested but cautious investors are waiting. Logically this will be at the top of the head of the 'head & shoulders' that shall not be named.

So back to my broker, my response was that I'm looking for the market to come back to the trend.

I will add to the short as the 'popular target' approaches. At its simplest, the short trade is looking for a move back to longer term support. If we break lower from there so be it. If, against the wash of fundamental data, the market finds legs, I'm happy to go with that too. My experience suggests there is a trade to be made from betting against the parabolic move...

Wednesday, September 16, 2009

The good and the bad

Following is a summary of the pressure points in the market over the nearish term. It's not intended to be exhaustive nor particularly prescriptive...more the impressionist in me trying to find expression (shudda picked up a paintbrush rather than a HP12C?).

.jpg)

The objective was to get some clarity around some of the path critical events that may or may not happen. For example:

.jpg)

The objective was to get some clarity around some of the path critical events that may or may not happen. For example:

- Liquidity tightened - is a near certainty in the near term. The Fed has $14.9 billion left in the POMO kitty. The Europeans remain as disfunctional and disjointed as ever, don't expect the ECB to keep underwriting the periphery indefinitively. The Chinese caused a tremor in their market when they hinted at tightening credit standards back in June. Question is whether the rally can sustain its bid without the cash injections?

- Banking regulations - mutterings from the G20 suggest consensus that banks will be required to hold more capital and more liquidity and be allowed less off balance sheet leverage. It may take some time to unfold but all these things work counter to the money multiplier and banking profits.

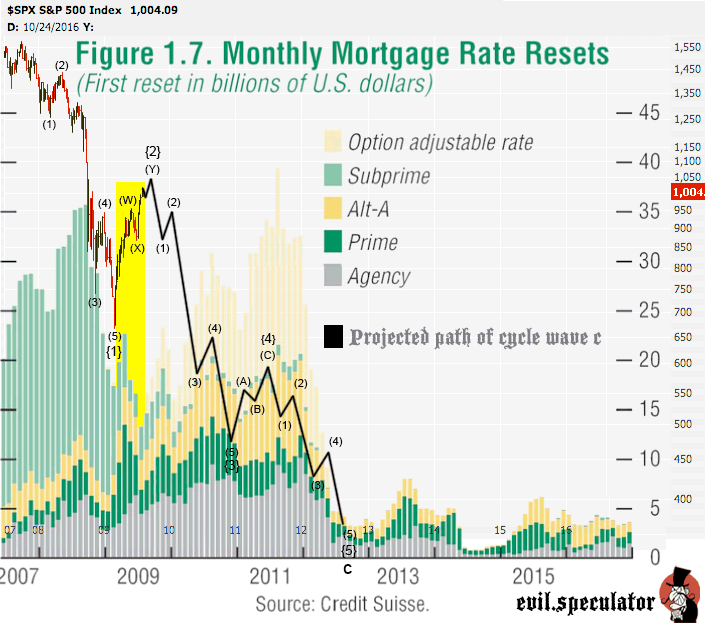

- US mortgage stress - Meredith Whitney is one of the clearest thinkers on the US banks and housing markets - she expects another 25% down in house prices with banks really struggling from here given they are at their reserve limits at current price levels. She observed that to date no one has been prepared to hit the bid - meaning that the state sponsored approach has been to paper over the problems and hope to maintain an orderly selldown. The implication is that this round (should it happen), there is a risk that the fire sales begin. The Evil Speculator has put together an interesting chart that shows the upcoming reset mountain (and his own interpretation of a snail crawling along a razor's edge).

- End of fiscal stimulus - Fiscal stimulus has probably peaked across the major economies (Cash for Clunkers ends and auto sales down in September, China steel prices down in September due to stockpiling for example). The strength of the rebound in economic activity will be tested as the fiscal stimulus rolls off - some like David Rosenberg say the recovery is all due to the fiscal measures.

- Bailout of Europe - the likes of Italy, Greece and Spain are truly pickled. The Euro might survive, but the political cohesion required to fund the bail-out of one or two of these countries will be something new for Europe. This is a reasonable likelihood and would not be good for the EUR.

- Eastern Europe collapse - probably more likely than not that one of the Baltic states will fold under its debt burdens or from civil unrest or maybe a combination of both. The Latvians must be pretty pissed that they are the only country around the world that is being subjected to the rack (while everyone else gets the fluffy pillow around the face treatment).

- China bubble - are we at the start of a bubble or the end of one? From this distance, and looking through the red veil, it's too bloody hard to tell. In the one camp, there are the likes of Andy Xie and on the other articles like this from Soc Gen (via The Pragmatic Capitalist).

- US government credibility fails - worst case scenario is that faith in the oval office fails and the USD makes a quantum leap into another universe. It's unlikely but possible - if the government keeps pumping in the cash like it has some. At the limit, the threat of this type of event will constrain US government actions (it's probably more likely that the government starts a new war).

- Loose monetary policy - zero interest rates for as far as the eye can see. If there is a hint of a self sustaining recovery, those companies that are positioned for it will enjoy low interest rates - both at the near and far end of the curves. Don't expect inflation until some of the world output gap has been closed.

- Corporate earnings - again companies that are able to leverage economic activity will benefit from rising productivity and lower labour unit costs. This is a good thing if you can get it.

- World GDP growth at 3% - Credit Suisse in a report published by TPC point to the arithmetic that would deliver the world GDP growth of around 3%. It rests on the emerging economies steaming ahead. If China can continue it's recent form who knows? They have deep pockets and like to build things...

Monday, September 14, 2009

It is liquidity driving the market

The economist David Rosenberg makes the headline statement in today's missive that "It's not liquidity driving the market". Rather than guess at his motivations - let's have a look at how liquidity is driving the market.

First up, define liquidity as referring to the relative ease with which an asset can be sold. Typically, selling an asset for cash is the most expedient way to realise an asset's value. In a sense, cash is the most liquid of assets (as a store of value its pretty darn good most of the time and everyone is happy to use it as a medium of exchange). For this reason, cash is at the very heart of the liquidity concept.

When there is an abundance of liquidity for a given asset, selling it can be achieved quickly and with minimum price disturbance to that asset. When there is an abundance of liquidity in an economy as a whole, there is lots of cash available to buy assets - it is relatively easy to sell assets across the risk spectrum.

From this definition, the impact of liquidity on markets seems straightforward. To get a sense of how it can be measured, a former roomie of Mr Rosenberg, Stephen Roach, points to a useful indicator:

My favorite gauge of the quantity dimension of liquidity is the so-called “Marshallian K” -- the difference between growth in the money supply and nominal GDP. In essence, this measures the surplus of money that is not absorbed by the real economy.

When the money supply is growing faster than nominal GDP, then excess liquidity tends to flow to financial assets. On the flip side, if money supply is growing more slowly than nominal GDP, then the real economy absorbs more available liquidity.

Under this model, asset price inflation will be the result of excess liquidity. For example have a look at some research from BCA on the correlation of the US$ gold price with the Marshallian K and then as compared to CPI:

Now while David makes the point that the Fed's most recent pumping of the monetary base has had little impact on broader money aggregates (as bank lending continues to contract at record rates), by taking a step back from the four week data we can see that the Fed has provided the system with a mountain of cash (charts from the St Louis Fed):

.jpg)

Conceptually, this view of liquidity helps explain how treasuries can continue to rally in tandem with equities markets and economic indicators pointing to a recovery (latest being the OECD leading indicators - have a look at the charts, there are some scary ones).

The conclusion - it may be an over-simplification to say "liquidity is driving the market", but as a generalisation it has greater merit than suggesting the opposite.

The actions of central banks around the world are predicated on the basis that they are enhancing liquidity. The objective might be to loosen up the money multiplier/creation process (not that they are necessarily having much luck on this front) but the effect is clearly being felt in asset prices. Banks may not be lending but they are investing all this cheap money they have been given in carry trades where ever they can find them.

Which leads us back to the question, where is liquidity going? - or rephrased, how long will governments continue with quantitative easing? The Fed has indicated a strategic withdrawal in October. Without the methyl, I'm expecting asset prices to correct...

First up, define liquidity as referring to the relative ease with which an asset can be sold. Typically, selling an asset for cash is the most expedient way to realise an asset's value. In a sense, cash is the most liquid of assets (as a store of value its pretty darn good most of the time and everyone is happy to use it as a medium of exchange). For this reason, cash is at the very heart of the liquidity concept.

When there is an abundance of liquidity for a given asset, selling it can be achieved quickly and with minimum price disturbance to that asset. When there is an abundance of liquidity in an economy as a whole, there is lots of cash available to buy assets - it is relatively easy to sell assets across the risk spectrum.

From this definition, the impact of liquidity on markets seems straightforward. To get a sense of how it can be measured, a former roomie of Mr Rosenberg, Stephen Roach, points to a useful indicator:

My favorite gauge of the quantity dimension of liquidity is the so-called “Marshallian K” -- the difference between growth in the money supply and nominal GDP. In essence, this measures the surplus of money that is not absorbed by the real economy.

When the money supply is growing faster than nominal GDP, then excess liquidity tends to flow to financial assets. On the flip side, if money supply is growing more slowly than nominal GDP, then the real economy absorbs more available liquidity.

Under this model, asset price inflation will be the result of excess liquidity. For example have a look at some research from BCA on the correlation of the US$ gold price with the Marshallian K and then as compared to CPI:

Now while David makes the point that the Fed's most recent pumping of the monetary base has had little impact on broader money aggregates (as bank lending continues to contract at record rates), by taking a step back from the four week data we can see that the Fed has provided the system with a mountain of cash (charts from the St Louis Fed):

US Adjusted Monetary base

.jpg)

Conceptually, this view of liquidity helps explain how treasuries can continue to rally in tandem with equities markets and economic indicators pointing to a recovery (latest being the OECD leading indicators - have a look at the charts, there are some scary ones).

The conclusion - it may be an over-simplification to say "liquidity is driving the market", but as a generalisation it has greater merit than suggesting the opposite.

The actions of central banks around the world are predicated on the basis that they are enhancing liquidity. The objective might be to loosen up the money multiplier/creation process (not that they are necessarily having much luck on this front) but the effect is clearly being felt in asset prices. Banks may not be lending but they are investing all this cheap money they have been given in carry trades where ever they can find them.

Which leads us back to the question, where is liquidity going? - or rephrased, how long will governments continue with quantitative easing? The Fed has indicated a strategic withdrawal in October. Without the methyl, I'm expecting asset prices to correct...

The real economy - trade flows

The timely and aggressive actions of governments around the world have seemingly averted disaster. A variety of economic indicators point to stabilisation, if not outright recovery. The liquidity that is sploshing around the global economy is finding its way into asset price inflation in an echo of the aftermath of the 1987 crash.

Is the global financial crisis over or is the real economic crisis just beginning? I'm gonna try to have a deeper look at the liquidity effect later in the week - today the focus is on trade as an indicator of the 'real economic' situation.

Question: why has the Baltic Dry Index dropped by ~40% since the start of June while the S&P500 has risen by 13% over the same period?

.jpg)

The BDI is a composite measure of worldwide shipping prices for dry bulk cargoes which comprise the majority of worldwide cargo traffic. It takes in 26 shipping routes and covers dry bulk barriers carrying a range of commodities (coal, iron ore and grain etc.). As the departure point for many a supply chain, it is often considered a leading indicator for industrial production and world economic growth.

While over the medium term, the BDI will be impacted by the supply side of the shipping equation (China likes building big boats - expect overcapacity to be visiting a port near you sometime soon) in the short term it is much more sensitive to simple demand and supply for the commodities being shipped.

In that context, you can clearly see the impact of the global government spending spree that commenced in late 2008. It's well documented that China was on a stockpiling binge over the first six months of 2009, which supports the ramp up in the BDI.

Then what? The party seems to have hit the wall.

While governments and brokers point to the turning up in GDP and industrial production numbers in developed countries, the BDI is suggesting the near term run-up in commodities trade volumes is done. This correlates with comments from the likes of BHP suggesting that China is finished stockpiling and hoping that Europe and the US take-up the slack in the form of re-stocking. In short, the BDI is not signalling confirmation that the developed world is doing anything but trying to find a bottom at vastly reduced trading levels.

Consider the following chart of world trade growth from the OECD Economic Outlook June 2009:

.jpg)

This translates to world trade growth projections like the following:

OECD forecasts for year-on-year changes in world trade volume for 2009: -12.0% and 2010: +5.5%

World Bank forecasts for year-on-year changes in world trade volume 2009: -9.7% and 2010: +3.8%

IMF forecasts for year-on-year changes in world trade volume 2009: -12.2% and 2010: +1.0%

I'll leave you to extrapolate your favourite forecast onto a chart of trade volumes (data from CPB Nederlands as at June 09):

.jpg)

The clear point from this is that world trade has fallen a long way, and while it may have turned up, it is unlikely to recover its peak for a considerable time.

And here we have one of the core problems facing the global economy. The trade imbalances that were financed by debt remain unresolved. Untangling these is likely to be a painful process.

Have a quick look at the breakup of export flows for some of the major economies from 2008 (UN data).

.jpg)

Ideally, I was going to match up against imports - but this piece has run over budget. However, some quick observations:

1) Germany is an exporting machine - but to Europe. The periphery figures highly as the importing counterpart (and it would have been financed on credit). Europe's trade imbalance hangs heavy over the future political stability of Europe and the Euro. It's one of the key potential positives for the USD.

2) Japan has developed a handy export business to China. It's been suggested that Japan may be one the key beneficiary's of the industrialisation of China in the long term. This hasn't stopped Japan from being severely hit by a drop in exports (~30%) that has triggered deflationary forces internally.

3) US relies on exports to Latin America and Canada. The relative under-performance of the USD versus these regions assists its export efforts in this respect. The problem is the import side of the ledger (not shown) where the US has been importing deflation. (See Albert Edwards chart.) It's just cheaper to get goods made in China (note that ~60% of China's trade surplus with the US comes from US companies that manufacture goods in China and then import into US).

4) China has built a diversified export empire. Amazing. But it remains dependent upon exports to support its economic growth model.

So not only is the trading pie getting smaller, the make-up of the pie is not conducive to a quick solution. The surplus trade economies remain hooked on exports. The deficit countries are tapped out, unwilling and unable to continue to buy whether from exporters or their own economies. The ideal objective is for the two to swap roles, at least for a little while. That is going to be tough.

Conclusions:

1) Expect 'protectionist' measures - resolving trade imbalances will be painful. In the debtor nation, it requires falling living standards and for open market economies like the US, higher unemployment. expect governments to come under increasing pressure to protect jobs and ensure that its spending stays at home (eg. US tariffs on steel and tires).

2) Expect surplus countries to export deflation - their economies are geared to exports. While China wants to increase its domestic consumption (36% of GDP), it will not happen overnight. Not only is China a big lender to the US, its biggest customer is the US. Chinese overcapacity will flow back into the US (and globally) as cheaper prices on goods (eg. steel into South Korea).

3) Expect China to buy the farm, not the produce. While the Chinese have been stockpiling industrial commodities in the first half, and this has propped up trade volumes, we can question the longevity of this strategy. It seems to me that they will be more inclined to buy the physical asset (the mine, the permit, the offtake agreement) than take the commodity out of the earth, ship it half way round the globe, just to have it sit in a warehouse. (China annexing parts of Africa when the locals revolt against perceived empiricism.)

Thursday, September 10, 2009

Get Shorty 2

Remain stubbornly of the view that another major leg down in the market is inevitable. But in a society where just-in-time means calling ahead to say you are running late, it's not surprising that us punctual types are always early.

Rather than re-run the many reasons as to why fundamentally, sentimentally and technically this rally should be very near its use-by date, I give you this chart:

.bmp)

I will add to shorts if and (more likely) when we get to the breakdown zone around 4680-4740. I'm expecting this resistance to hold first-up and, perhaps in tune with the prospect of index selling next week, wouldn't be surprised to at least see a retracement to 4460/80.

From there depends on how the top plays out. On balance, given the strength of this move, the base case should be a parabolic blow-off to 5000 through October.

My thinking is that the market could turn on a dime at any time. Hence the core short position. But for a near term reversal to happen it requires a catalyst (a sovereign default in Europe for example). Given the internals of this market are built out of genetically modified straw, the spark does not have to be big (a small sovereign state default then?).

However, in the absence of a catalyst, a top is more likely to be found through sheer toe-curling exhaustion. 5000 is the level to target here. It's a 50% retracement of the whole down move. It balances the A and C waves nicely. It's a lovely round number. It would make for a nice view over the edge for a traditional October wipe-out. Really, the only reasons I can come up with are technical cause everything else points down - now.

Rather than re-run the many reasons as to why fundamentally, sentimentally and technically this rally should be very near its use-by date, I give you this chart:

.bmp)

I will add to shorts if and (more likely) when we get to the breakdown zone around 4680-4740. I'm expecting this resistance to hold first-up and, perhaps in tune with the prospect of index selling next week, wouldn't be surprised to at least see a retracement to 4460/80.

From there depends on how the top plays out. On balance, given the strength of this move, the base case should be a parabolic blow-off to 5000 through October.

My thinking is that the market could turn on a dime at any time. Hence the core short position. But for a near term reversal to happen it requires a catalyst (a sovereign default in Europe for example). Given the internals of this market are built out of genetically modified straw, the spark does not have to be big (a small sovereign state default then?).

However, in the absence of a catalyst, a top is more likely to be found through sheer toe-curling exhaustion. 5000 is the level to target here. It's a 50% retracement of the whole down move. It balances the A and C waves nicely. It's a lovely round number. It would make for a nice view over the edge for a traditional October wipe-out. Really, the only reasons I can come up with are technical cause everything else points down - now.

Wednesday, September 9, 2009

Internal devaluation defined

There is a certain symmetry to the Swedish oeuvre - boxy Volvo's, Bjorn Borg's headband, ABBA's white jumpsuits, losing the kids in Ikea...and now 'internal devaluation'.

It's a term that appears to be gaining some traction (albeit that it is yet to register a tremor on the Google Trends richter scale). I wouldn't be surprised to hear it used by mainstream media in relation to the US-China relationship sometime soon.

If it sounds like an oxymoron that's because, strictly speaking, it is. (Perhaps that is why I like it so.) 'Devaluation' refers to a process whereby a certain thing reduces in value relative to another thing - by definition this other thing is external to the first. It typically refers to a country's currency reducing in value relative to others.

The Swedes first coined the phrase back in the late 90's when exploring mechanisms to manage their economy should they join the Euro. It has gained in prominence in recent times as a way to describe the adjustment process that Latvia has adopted to gain access to IMF supported funding. No surprise that Swedish banks are the biggest creditors to Latvia.

Anyway, the essential thrust of the concept is that a country in a fixed exchange rate regime can still manage its relative competitiveness by reducing its labour costs through fiscal measures. For example, a country could finance a decrease in payroll taxes through increased income taxes. Such a shift reduces real labour costs and therefore increases the competitiveness of exports - while also being budget neutral and reducing consumer demand in that country. In theory, it therefore achieves a similar outcome as a currency devaluation. (And to be fair, as the objective is to reduce the labour costs relative to that country's trading partners, there is some internal logic to calling it an internal devaluation.)

In Latvia's circumstances, it seems that the term has departed somewhat from its original meaning. The IMF sponsored plan calls for 20% cuts in public sector wages, 20% cuts in pensions, an increase in VAT from 21% to 23%, rises in the average effective rate of personal income tax etc... There isn't much focus on labour productivity or unit costs. It's simply reduce the budget deficit at all costs.

From this distance (which admittedly is a long way) it seems that Latvia has been bent over in an attempt to save some of those Swedish bank loans - there is a general consensus that a devaluation of its currency would wipe out a great swathe of what's left of the private sector given the impact this would have on EUR denominated debt.

The people of Latvia aren't happy.

Now while this is all very interesting (or not) what has it to do with the price of fish (outside Riga)? The answer is that some pretty important currency relationships around the world are effectively fixed - think the EUR countries and the exchange rate between the US and China. And some of the countries in these relationships are straining from imbalances similar to those that have impacted Latvia.

Consider the US-China pairing. A Fistful of Euros has already suggested that China has applied its own unique brand of 'internal revaluation'. Rather than let the RMB appreciate, it will apply 'rebalancing measures' to increase domestic consumption by increasing social security and healthcare benefits (thereby increasing disposable income as consumers don't have to save for emergencies).

And to flip it around the other way, with China pegging the RMB to the USD, the US is faced with the same obstacles in trying to engineer greater competitiveness for its goods. It's market can respond in the only way it can - increase the ranks of the army of the unemployed, thereby forcing labour market reform. I can almost hear Keating saying "It's the internal devaluation we had to have"...

The funny thing is that the US is doing the exact opposite of the IMF prescribed medicine for Latvia. Everyone knows that there is a logical limit to the amount of debt the government can issue...the question remains how close are we to it?

It's a term that appears to be gaining some traction (albeit that it is yet to register a tremor on the Google Trends richter scale). I wouldn't be surprised to hear it used by mainstream media in relation to the US-China relationship sometime soon.

If it sounds like an oxymoron that's because, strictly speaking, it is. (Perhaps that is why I like it so.) 'Devaluation' refers to a process whereby a certain thing reduces in value relative to another thing - by definition this other thing is external to the first. It typically refers to a country's currency reducing in value relative to others.

The Swedes first coined the phrase back in the late 90's when exploring mechanisms to manage their economy should they join the Euro. It has gained in prominence in recent times as a way to describe the adjustment process that Latvia has adopted to gain access to IMF supported funding. No surprise that Swedish banks are the biggest creditors to Latvia.

Anyway, the essential thrust of the concept is that a country in a fixed exchange rate regime can still manage its relative competitiveness by reducing its labour costs through fiscal measures. For example, a country could finance a decrease in payroll taxes through increased income taxes. Such a shift reduces real labour costs and therefore increases the competitiveness of exports - while also being budget neutral and reducing consumer demand in that country. In theory, it therefore achieves a similar outcome as a currency devaluation. (And to be fair, as the objective is to reduce the labour costs relative to that country's trading partners, there is some internal logic to calling it an internal devaluation.)

In Latvia's circumstances, it seems that the term has departed somewhat from its original meaning. The IMF sponsored plan calls for 20% cuts in public sector wages, 20% cuts in pensions, an increase in VAT from 21% to 23%, rises in the average effective rate of personal income tax etc... There isn't much focus on labour productivity or unit costs. It's simply reduce the budget deficit at all costs.

From this distance (which admittedly is a long way) it seems that Latvia has been bent over in an attempt to save some of those Swedish bank loans - there is a general consensus that a devaluation of its currency would wipe out a great swathe of what's left of the private sector given the impact this would have on EUR denominated debt.

The people of Latvia aren't happy.

Now while this is all very interesting (or not) what has it to do with the price of fish (outside Riga)? The answer is that some pretty important currency relationships around the world are effectively fixed - think the EUR countries and the exchange rate between the US and China. And some of the countries in these relationships are straining from imbalances similar to those that have impacted Latvia.

Consider the US-China pairing. A Fistful of Euros has already suggested that China has applied its own unique brand of 'internal revaluation'. Rather than let the RMB appreciate, it will apply 'rebalancing measures' to increase domestic consumption by increasing social security and healthcare benefits (thereby increasing disposable income as consumers don't have to save for emergencies).

And to flip it around the other way, with China pegging the RMB to the USD, the US is faced with the same obstacles in trying to engineer greater competitiveness for its goods. It's market can respond in the only way it can - increase the ranks of the army of the unemployed, thereby forcing labour market reform. I can almost hear Keating saying "It's the internal devaluation we had to have"...

The funny thing is that the US is doing the exact opposite of the IMF prescribed medicine for Latvia. Everyone knows that there is a logical limit to the amount of debt the government can issue...the question remains how close are we to it?

Monday, September 7, 2009

DJ MARKET TALK: FTSE Downweight May Weigh On S&P/ASX 200

Been trying to get to the bottom of the following snippet that was published on September 3...

0336 GMT [Dow Jones] FTSE Developed Asia Pacific ex-Japan downweight of Australian

equities, resulting from addition of South Korea on Sep. 18, may see up to A$5 billion

worth of funds removed from Australian equities, according to traders and strategists.

Australia's weighting in the index will fall by 9.1 percentage points to 45.82%.

Goldman Sachs JBWere estimates this will generate passive fund outflows of A$600 million

and active fund outflows of A$4 billion. Expects selldown in Australian equities through

Sep. 14-18.

The announcement of the promotion of South Korea from 'Advanced Emerging' to full blooded 'Developed' was made in September last year. The effective date for the change is the close of business on 18Sep09 - so index followers presumably are going to reduce their holdings in a manner that will best match the performance of the index to that date - hence the expected selling 14 through to 18 September.

To give you a context, here are FTSE's classification of Asia-Pacific countries:

Developed - Australia, HK-China, Japan, NZ, Singapore

Advanced emerging - Malaysia, South Korea, Taiwan

Secondary emerging - China, India, Indonesia, Pakistan, Phillipines, Thailand

The rather specialised FTSE Developed Asia ex-Japan index had 287 constituents and a market capitalisation of US$1,418bn as at 31Aug09. Note that 'red chip' shares listed in Hong Kong are also to be reclassified as 'China' effective 18 Sept.

Australia (apparently) makes up 55% of the index or ~A$920bn (which compares to a market capitalisation for the All Ordinaries on the same date of $1,265bn and for the ASX200 of around $1,010bn).

If a 9.1% fall in the index weighting approximates to A$5bn, this implies that FTSE index followers have A$55bn in current holdings in the Australia (or 6% of the index defined universe). Not sure how the likes of Goldman and AMP have calculated the ~$5bn number - but it seems broadly plausible.

Without obtaining the exact index composition from FTSE, we can assume that it broadly reflects that of S&P200. The banks and major mining companies will dominate, while property outside the heavyweights will be a rounding error.

Is $5bn a meaningful number then? Well, daily turnover of the S&P200 is typically in the $3bn to $5bn range. So the short answer is yes, if the value of shares to be sold is in the order of $5bn it would represent a material amount of weekly volume (call it 20%).

As a cross check consider the volume of secondary issuance by month - note that the market has run higher in recent times against a rising tide of issuance (mind you a lot of this supply has been issued at discounts to prevailing market prices).

.jpg)

In summary, if index followers will be selling circa $5bn shares in the week ending September 18, expect the market to be a little soft at that time...

Postscript:

A couple of further thoughts on the $5bn figure

1) The reweighting will only lead to selling where a fund manager is wholly beholden to the index (eg. $100m fund that is benchmarked to the index). If a fund manager follows this index amongst others in its universe (eg. a sovereign wealth fund), then the reweighting may simply lead to a reallocation between indices (South Korea drops out of one and reappears in another). As a somewhat esoteric index in isolation, this must be relevant to some funds - which leads to the next point...

2) I have not come across any funds that are specifically benchmarked to this index. Typically, a MSCI index is used by fund managers in this region - at least in the retail funds management space. Probably doesn't say much as it is not as if I have done extensive studies on fund manager benchmarking.

The point is to take the $5bn with a grain of salt. I have taken Goldman's conclusions at face value.

0336 GMT [Dow Jones] FTSE Developed Asia Pacific ex-Japan downweight of Australian

equities, resulting from addition of South Korea on Sep. 18, may see up to A$5 billion

worth of funds removed from Australian equities, according to traders and strategists.

Australia's weighting in the index will fall by 9.1 percentage points to 45.82%.

Goldman Sachs JBWere estimates this will generate passive fund outflows of A$600 million

and active fund outflows of A$4 billion. Expects selldown in Australian equities through

Sep. 14-18.

The announcement of the promotion of South Korea from 'Advanced Emerging' to full blooded 'Developed' was made in September last year. The effective date for the change is the close of business on 18Sep09 - so index followers presumably are going to reduce their holdings in a manner that will best match the performance of the index to that date - hence the expected selling 14 through to 18 September.

To give you a context, here are FTSE's classification of Asia-Pacific countries:

Developed - Australia, HK-China, Japan, NZ, Singapore

Advanced emerging - Malaysia, South Korea, Taiwan

Secondary emerging - China, India, Indonesia, Pakistan, Phillipines, Thailand

The rather specialised FTSE Developed Asia ex-Japan index had 287 constituents and a market capitalisation of US$1,418bn as at 31Aug09. Note that 'red chip' shares listed in Hong Kong are also to be reclassified as 'China' effective 18 Sept.

Australia (apparently) makes up 55% of the index or ~A$920bn (which compares to a market capitalisation for the All Ordinaries on the same date of $1,265bn and for the ASX200 of around $1,010bn).

If a 9.1% fall in the index weighting approximates to A$5bn, this implies that FTSE index followers have A$55bn in current holdings in the Australia (or 6% of the index defined universe). Not sure how the likes of Goldman and AMP have calculated the ~$5bn number - but it seems broadly plausible.

Without obtaining the exact index composition from FTSE, we can assume that it broadly reflects that of S&P200. The banks and major mining companies will dominate, while property outside the heavyweights will be a rounding error.

Is $5bn a meaningful number then? Well, daily turnover of the S&P200 is typically in the $3bn to $5bn range. So the short answer is yes, if the value of shares to be sold is in the order of $5bn it would represent a material amount of weekly volume (call it 20%).

As a cross check consider the volume of secondary issuance by month - note that the market has run higher in recent times against a rising tide of issuance (mind you a lot of this supply has been issued at discounts to prevailing market prices).

.jpg)

In summary, if index followers will be selling circa $5bn shares in the week ending September 18, expect the market to be a little soft at that time...

Postscript:

A couple of further thoughts on the $5bn figure

1) The reweighting will only lead to selling where a fund manager is wholly beholden to the index (eg. $100m fund that is benchmarked to the index). If a fund manager follows this index amongst others in its universe (eg. a sovereign wealth fund), then the reweighting may simply lead to a reallocation between indices (South Korea drops out of one and reappears in another). As a somewhat esoteric index in isolation, this must be relevant to some funds - which leads to the next point...

2) I have not come across any funds that are specifically benchmarked to this index. Typically, a MSCI index is used by fund managers in this region - at least in the retail funds management space. Probably doesn't say much as it is not as if I have done extensive studies on fund manager benchmarking.

The point is to take the $5bn with a grain of salt. I have taken Goldman's conclusions at face value.

Eats, Shoots and Leaves - the evolution of the 'green shoots' cliche

There is a lot to be said for studying the entrails of the financial media. Sentiment drives markets and there is no doubting that the media has a role to play in nurturing sentiment. (Whether it is a contrarian indicator is an argument for another day.)

Take for example, the phrase 'green shoots'. Following is a chart from Google Trends that maps the search volume for the term over time.

i) The evolution of the phrase into a fine upstanding cliche began way back in 1991 when the then Chancellor Lamont heralded the 'green shoots of economic spring' (see the relevant snippet on BBC). On this basis, we should give proper credit to Lord Lamont - well done - even if it cost you your job.

ii) In January 2009, the phrase was picked up by ITV and thrown into a question put to a UK minister, Baroness Vadera (see the snippet here). She took the bait, hook-line-and-sinker, and soon found herself the subject of much criticism. (You must really marvel at the evil intelligence of the UK's media machine.) No surprise then that politicians were not seeing anything remotely green from then on.

iii) It took a non-elected government official to resurrect the phrase in March 2009. Ben Bernanke saw some green shoots in an interview on 60 Minutes (get the whole CBS experience here). It speaks volumes for the nature of the crisis that it is a central banker that is defining the popular mood (not that it is a new thing in the US - think 'irrational exuberance' - just its not really 'democracy' is it?).

After that things rapidly gained momentum. What the US media machine lacks in Machiavellian smarts it makes up for in raw enthusiasm. It hammered the green shoots line without mercy.

iv) By June, 'green shoots' had reached cliche nirvana. Everyone in the english speaking world had said the phrase at least once. In Paris, university students joined with government think-tanks to develop strategies to defend their borders. Typically, Warren Buffett had the pithiest comment (June 24):

“We’re not seeing them,” Buffett said on CNBC. “I had a cataract operation in my left eye about a month ago and I thought, maybe now I’ll be able to see some green shoots.”

Enough already - you get the point. All the while the credit and equity markets have been rallying, the media has been plugging the green shoots line. I'm not arguing cause and effect here - it's probably mutually reinforcing.

Anyway...what got me going on all this was the thought that there has been a subtle shift in media and broker speak about what the world expects from China and emerging markets generally. The 'decoupling' theory that was popular around the middle of 2008 - that suggested that these markets would not be affected by the recession in the US and Europe - has been replaced with the 'yet-to-be-labelled' theory that has China at the very centre of the world economic recovery.

The new theory started to emerge around the time that 'green shoots' grabbed for its 15 minutes in the sun. (For example see Decoupling 2.0 from the Economist in May 2009). While it may never gain the traction of 'green shoots', I have the sense that this 'China will lead out us all out of recession' meme is important to the overall stability of this rally. More on this later...

Take for example, the phrase 'green shoots'. Following is a chart from Google Trends that maps the search volume for the term over time.

i) The evolution of the phrase into a fine upstanding cliche began way back in 1991 when the then Chancellor Lamont heralded the 'green shoots of economic spring' (see the relevant snippet on BBC). On this basis, we should give proper credit to Lord Lamont - well done - even if it cost you your job.

ii) In January 2009, the phrase was picked up by ITV and thrown into a question put to a UK minister, Baroness Vadera (see the snippet here). She took the bait, hook-line-and-sinker, and soon found herself the subject of much criticism. (You must really marvel at the evil intelligence of the UK's media machine.) No surprise then that politicians were not seeing anything remotely green from then on.

iii) It took a non-elected government official to resurrect the phrase in March 2009. Ben Bernanke saw some green shoots in an interview on 60 Minutes (get the whole CBS experience here). It speaks volumes for the nature of the crisis that it is a central banker that is defining the popular mood (not that it is a new thing in the US - think 'irrational exuberance' - just its not really 'democracy' is it?).

After that things rapidly gained momentum. What the US media machine lacks in Machiavellian smarts it makes up for in raw enthusiasm. It hammered the green shoots line without mercy.

iv) By June, 'green shoots' had reached cliche nirvana. Everyone in the english speaking world had said the phrase at least once. In Paris, university students joined with government think-tanks to develop strategies to defend their borders. Typically, Warren Buffett had the pithiest comment (June 24):

“We’re not seeing them,” Buffett said on CNBC. “I had a cataract operation in my left eye about a month ago and I thought, maybe now I’ll be able to see some green shoots.”

Enough already - you get the point. All the while the credit and equity markets have been rallying, the media has been plugging the green shoots line. I'm not arguing cause and effect here - it's probably mutually reinforcing.

Anyway...what got me going on all this was the thought that there has been a subtle shift in media and broker speak about what the world expects from China and emerging markets generally. The 'decoupling' theory that was popular around the middle of 2008 - that suggested that these markets would not be affected by the recession in the US and Europe - has been replaced with the 'yet-to-be-labelled' theory that has China at the very centre of the world economic recovery.

The new theory started to emerge around the time that 'green shoots' grabbed for its 15 minutes in the sun. (For example see Decoupling 2.0 from the Economist in May 2009). While it may never gain the traction of 'green shoots', I have the sense that this 'China will lead out us all out of recession' meme is important to the overall stability of this rally. More on this later...

Sunday, September 6, 2009

The 8 Reasons Goldman Sachs says buy the Chinese Sell-Off

The Pragmatic Capitalist has published a summary of a recent Goldman Sachs report (TPC's article here) that suggests they are bullish on China.

Perhaps it's time to change my medication - give me whatever Goldies are having - the blue pills? - great and my favourite colour too.

I have already commented on TPC's site, so won't rehash the specifics here - suffice to say we have diametrically opposite views.

Perhaps it's time to change my medication - give me whatever Goldies are having - the blue pills? - great and my favourite colour too.

I have already commented on TPC's site, so won't rehash the specifics here - suffice to say we have diametrically opposite views.

Friday, September 4, 2009

.jpg)

Thursday, September 3, 2009

Steel as a proxy for BHP

Getting back to my ruminations of a couple of days ago – want to explore the world of BHP a little more.

BHP – broker consensus has it a BUY?

While some naysayers in the broker community have deemed BHP a ‘Hold’, the majority of the professional pundits rate it a ‘Buy’. The investment thesis is broadly based on the principles that:

1) The developed world has turned the corner, and therefore will resume its demand for commodities,

2) China’s economy has gathered a ‘fresh head of steam’, and,

3) Medium to long-term commodity demand is underwritten by China’s industrialisation.

Simple enough, and certainly fits with the ‘recession is over’ theme.

While I’m not going to build a full-blown model for the mining behemoth, I think we can have a closer look at this consensually conceived thinking. Let’s take one analyst’s forecasts as a guide. Following is a summary of earnings (EBIT) by division:

Some quick observations on the three-year outlook:

- Petroleum remains a strong contributor on rising volumes

- Base metals make a resurgence with greater volumes

- Carbon steel remains the stand-out contributor, after a weaker 2010 reflecting lower prices/higher costs, volume and price picks up again into 2012

- Steaming coal takes a hit on lower prices in 2010 and kicks up again thereafter on rising volumes and prices

No sign of a global recession there - volumes just going to keep heading higher. And a similar story with the price assumptions behind these forecasts:

There you have it – volumes rise and so do prices. Couldn’t have asked for more. But before we boldly embrace the broker recommendation, let’s test the investment thesis using steel as the divining stick (particularly given it is so important to BHP’s earnings).

China’s insatiable demand for all things steel

Consider the following profile of world steel production since 2003 (from the World Steel Association):

First conclusion is that non-China production has fallen into a ditch. While it may be climbing from this lower base, it would be fanciful to assume that it is going to reclaim its pre-crash levels anytime in the near future. Just as construction activity in the developed world benefited from the debt inspired binge, it will struggle along with the chastened consumer in an extended period of fasting. On this basis, it’s probably not a great idea to hang your hat on the premise that the non-China world is going to drive growth in world steel production.

Not to worry though cause China has taken up the slack. As of July 2009, it accounts for approximately 50% of world steel production up from 5% in the early 1980’s. And while the 2008 year was a slow one by its usual standards (annual growth of only 1% in production volume), 2009 promises to be the harbinger of things to come with at least 10% annual growth seemingly in the bag.

So to support the broker assumptions of growing volume and prices, we only need to look to China’s steel production that will keep growing by 10% to 15% per annum for at least the next 10 years …right? (Small detail that is beyond my scope here – but the broker in question assumes BHP increases sale volumes of iron ore by more than 20% per annum from 2009 to 2012. Well, if the big Australian can’t grow its market share, who can?)

I reckon this scenario is a little optimistic for the following reasons:

1) China’s internal demand for steel has peaked - We have just witnessed an extraordinary capital injection from the government. With in excess of 60% of the fiscal package being directed towards infrastructure, and assuming an implied steel content of capital of around 15%, you can pretty quickly see how the recent surge in steel production has come about (and for that matter every other raw material that could be tucked away in a warehouse somewhere). Without a further impetus from the government (which is not out of the question), it will be a while before the level of internal demand is bettered.

2) China is an exporter of steel with no markets to export to – what the chart of world steel production doesn’t tell you, is the fact that until recently China has been a net exporter of steel (in fact the world’s largest). It’s conversion into a net importer wasn’t by choice, as the following chart from the Iron and Steel Statistics Bureau shows:

With the impact of the fiscal support fading, we are about to find out what the ‘real’ internal Chinese demand for steel is. The question then becomes what happens to the surplus capacity?

One answer may be that steel producers that would otherwise export product may get government assistance to reignite their export markets. Consider for example, the announcement on 8 June 2009 that the government will refund the 9% value-added tax rebate on exports of several high-end steel products. This is aimed at effectively undercutting the pricing of Posco in its own market (South Korea was the biggest importer of Chinese steel).

In short, I suspect that we are about to get a clearer picture about the real demand and supply of the Chinese steel industry (granted it will probably have vasoline smeared across the lense but at least the lense-cap will be off). On current indications, it looks less than supportive for an investment thesis that rests on double-digit growth in Chinese steel production over the next few of years.

3) China will gain pricing power – China’s steel industry struggles against persistent overcapacity (it produced 500mt in 2008 against a capacity at the time of around 600mt) that is spread across a plethora (72) of small and mid-sized producers. This creates an industry that is particularly vulnerable to demand and supply shocks. The flipside to the recent fiscally inspired boom is that once it is has passed, producers need to be weaned off the assistance. In an environment where export markets are particularly hard to find, it’s not surprising to hear reports of rapid stockpiling.

If you add into the mix that China’s producers operate on relatively thin average margins of around 5.5% (according to IMF working paper “Is China’s Export Oriented Export Growth Sustainable Aug-09) then there are all the ingredients for consolidation of the industry if it comes under stress. Hence, the statement from the China Mining Association that the industry lost money in the first four months of this year has special resonance. If you don’t believe me, have a look to the CISA for the direction that this is taking:

From China Steel and Iron Association on 31 July, 2009 – Secretary General of CISA suggested that steel makers accept a single ore price…to regulate excess ore shipments by small steel makers and intermediary traders, which have hampered negotiations by creating unnecessary demand.

(And for a little bit more colour on industry consolidation China style have a quick look at the state sponsored takeover of Rizhao Iron & Steel by Shandong Iron & Steel.)

It is highly likely that the likes of BHP can’t continue to make out like bandits, while the world's steel industry struggles with excess capacity. Expect consolidation in China's industry to deliver cohesive negotiating positions and pricing power – input prices will share in the pain of the ‘transition process’.

In summary, this doesn’t sound like a glowing endorsement of a financial model that suggests 20% per annum growth in volumes over the next 3 years as well as rising prices. As a litmus test for the investment thesis, it’s coming up red (or is it purple?).

What this discussion does throw into stark relief is the implicit reliance that world economic growth has on that red-lacquered flight-box China. The accepted wisdom is that we can rely on China to continue to grow at 8% per annum – cause without this there will be rioting and pillaging on its streets. There’s bound to be some truth in the myth, but as with all things, the truth is a whole lot more complicated. My take on it is that China may well continue to grow at 8% per annum, but in the current environment this may not translate to higher prices, perhaps not even higher volumes, for the likes of BHP.

I know this has been rather long but couldn’t leave the following out as I think steelprices-china.com summarises the current market with a certain panache…

The main reason of arousing price decline is that traders and speculators’ selling lead to low market expectation. Because of the overcapacity, once the downstream demand fluctuates, it will increase the stock. According to the present, the steel stock will still increase in few weeks.”

The report then goes on to point out how critical the recovery in the US is….

More and more professionals believe that market risk is increasing. Steel enterprises, traders and end users all think that it will have a big change on September in China’s steel market. There is an important mark is that the change of American economic data in third quarter as American economic recovery is the prerequisite of the global economic recovery. If American economic indicator of third quarter is improved, it will be a huge inspiration to Chinese economy even the whole world. Demand of steel and steel price will increase. Otherwise, the steel price will drop severely.

Wednesday, September 2, 2009

The liquidity trade is dead - long live the short commodities trade

We are witnessing a change in trend. The liquidity inspired rally of all things risk has bumped into the ceiling. Now the reality of a serious retrenchment in consumer demand is likely to take over as the cause celebre. Expect commodity prices to bear the brunt of this...

First to the signs that the liquidity trade is over (it's all ETF's today as a quick snapshot). Financials are starting to struggle:

First to the signs that the liquidity trade is over (it's all ETF's today as a quick snapshot). Financials are starting to struggle:

While Investment grade corporates outperform their slack-jawed cousins in hi-yield land - suggesting that the holders of investable cash aren't all that keen on the risk/reward for pushing up the risk spectrum.

And commodities? Oil has broken its uptrend...

Base metals are fluffing...

While gold is playing the fiddle...

Really not sure what to make of this break-out in gold given that hedge funds already have their pockets full of the stuff and everyone else has been waiting to play the break when it happens. Regardless wouldn't be surprised if there is some stop hunting to the downside.

Tuesday, September 1, 2009

What joy the State Street Confidence Index bringeth

It's been a while since having a gander at this sentiment index - and isn't it looking the picture of health!

.jpg)

.jpg)

Subscribe to:

Posts (Atom)

{kind=link}